LD Capital: Business Logic of DWF and How to Utilize Relevant Information to Guide Secondary Market Trading

Introduction

This year, DWF has risen to fame, with continuous large investments and tokens related to it often doubling in value. How has DWF achieved this even during the deep bear phase of the current crypto market? How should secondary market investors engage with the relevant subjects?

Summary

DWF is a product born in a bear market under weak supervision, capitalizing on the dilemmas of project teams and the psychology of retail investors in the market to profit from both ends. In the bear market, project teams commonly face difficulties in cashing out and financing. Directly selling tokens would strike a blow to the fragile market confidence, seriously depress token prices, and affect the project ecosystem. In this context, DWF emerges as a bridge for project teams to sell tokens, assisting them in selling through OTC or other marketing means. For instance, describing the behavior of OTC tokens from project teams as strategic investment, in reality, no substantial assistance to the project’s long-term development is observed; instead, they turn around and sell the tokens. By disguising the nature of the project teams’ indirect sell-off through promotional packaging, DWF also profits from both the project teams and the market in this process.

For secondary market investors, upon seeing information about a project’s collaboration with DWF, it is crucial first to distinguish what kind of business it pertains to with DWF (secondary investment, OTC, market-making, marketing) and to employ different strategies for different businesses. From past market performances:

1. Subjects of DWF’s direct participation in secondary market investments need special attention; these usually are new coins with good chip structures listed on exchanges or Memes.

2. Subjects from which DWF buys tokens OTC from project teams (packaged as strategic investments) tend to first show a decline in secondary market prices for several months, followed by a rapid upswing, ending after DWF deposits to exchanges (the upswing typically lasts no more than one week).

3. DWF’s actual market-making projects do not have doubling scenarios but often attract speculative capital, with brief windows for position building, capturing early advantages.

4. The success rate and profitability from surges caused by DWF-related marketing news are relatively poor, the underlying logic being interested parties using DWF’s current market influence to attract liquidity for dumping. After determining DWF’s intention to pump, the explosive increase in related contract positions and spot transaction volumes signals the start of the trend; interactions between DWF’s on-chain addresses and exchange addresses (at high prices), decreasing holdings, and extremely negative funding rates often indicate the end of the trend.

Main Text

DWF Labs, a subsidiary of Digital Wave Finance (DWF), is a global cryptocurrency high-frequency trading firm engaged in spot and derivative trading on over 40 top trading platforms since 2018. DWF Labs initially debuted in the crypto market as a market maker. The market’s real attention was drawn to DWF beginning in the first quarter with Hong Kong concept coins like CFX and ACH experiencing sharp increases, to the second quarter with MEME coins like PEPE and LADYS surging by dozens of times, and to recent listings like YGG and CYBER that have seen multiple increases in value. Among these, CFX, ACH, and YGG were acquired via OTC. Due to their good chip structures, coins like PEPE (MEME), LADYS (MEME), CYBER (Binance Launch Pool), etc., were purchased directly through secondary markets by DWF, influencing prices.

Tokens Related to DWF Experience Several-Fold Increase, Attracting Market Attention

The surge in tokens associated with DWF has caught the market’s eye. The attention DWF commands is due not only to the significant price fluctuations of the cryptocurrencies it handles but also to its discord with other industry counterparts. Renowned market makers like Wintermute and GSR have publicly expressed their dissatisfaction with DWF, labeling it a subpar market maker and a negative influencer within the industry.

Dissecting DWF’s Business Scope:

In the crypto market, investing and market making are typically two distinct concepts. Investing usually refers to providing financial support to teams for development, operations, and marketing before the token launch, with the reward being a share of the tokens with a lock-up period once the project goes live. Market making, on the other hand, aims to establish healthy liquidity for already-launched tokens, reduce transaction costs, and attract more traders. The returns on investment come from the token rewards of the invested project, while market-making profits come from fees paid by the project and the spread earned during the process. Notable investment entities in the crypto market include A16Z and Paradigm, while prominent market makers include Wintermute and GSR, among others.

DWF has been criticized by crypto market participants for often blurring the lines between investing and market making. On its official website, DWF positions itself as a Web3 venture capitalist and market maker, with business types divided into three categories: investing, OTC, and market making.

A retrospective view of DWF’s past performance shows a preference for emotionally charged themes, with market-making efforts spanning cryptocurrencies like CFX, MASK, YGG, C98, WAVES, and others. However, a closer examination of its past market-making ventures reveals scant genuine support for the long-term growth of projects. DWF typically opts to inject funds into “distressed” projects that have already launched tokens, acquiring tokens at a discount, and later selling them on secondary markets for a profit. Furthermore, it often manipulates the market aggressively for its “investments,” creating an image of profitability among retail investors, beyond just selling tokens at high prices. This image is then sold as a product to project owners. For example, by disclosing substantial investment information in conjunction with project owners, DWF creates market optimism, attracting liquidity for better token sales.

Apparent Business Activities: Investment, Market Making, OTC, Marketing

Core Business Nature: Injecting funds into “distressed” projects, acquiring tokens at OTC discounts, profiting from sales in secondary markets; aggressive market manipulation to build a brand image, and continuing to sell that image as a product to project owners.

Detailed case studies are as follows (to be continued with specific examples):

1. YGG & C98: Over-the-Counter (OTC) Coin Purchases and Secondary Market Price Manipulation for Offloading

On February 17, 2023, the blockchain gaming guild Yield Guild Games (YGG) raised $13.8 million through the sale of tokens, with DWF Labs and A16Z leading the investment (noting that YGG had already launched its token back in 2021).

What is noteworthy is that DWF Labs had already received 8 million YGG tokens from the YGG treasury on February 10th. They first transferred 700,000 of these tokens to Binance on February 14th. Then, on February 17th, the media reported on the investment information. Subsequently, DWF made two more transfers: 3.65 million tokens to Binance on June 19th and another 3.65 million on August 6th. Considering YGG’s price performance: influenced by the investment news on February 17th, YGG surged by as much as 50% during the day, closing 33% higher. However, this was followed by a decline that lasted five and a half months, until the market rebounded in early August. YGG’s value then increased more than sevenfold from its previous low by the time the market rally ended, coinciding with DWF’s last transfer of YGG tokens into Binance.

For secondary market investors, anomalies in contract data could have been observable at the onset of YGG’s market rally. YGG’s contract data initially showed a sharp increase in open interest and stable fees. This was followed by a slowdown in the growth of open interest, a reduction in fees mid-way, and eventually, a decrease in open interest due to longs unwinding their positions.

Similar trading maneuvers can also be observed in subjects like CYBER: On August 22, DWF withdrew 170,000 CYBER from the Binance exchange when the price of CYBER was approximately $4.5. Subsequently, the price consistently fell, reaching a low of $3.5. Seven days later, a CYBER price increase commenced, peaking at $16.2. This was about a 3.6-fold increase from the price when DWF withdrew its tokens and about a 4.6-fold rise from the previous low. As a Binance Launch Pool project, CYBER had a favorable chip structure in its early days after launch, leading to minimal sell-off pressure in the secondary market. It is inferred that DWF’s participation in CYBER was mainly through secondary market purchases to prop up the price, with less involvement concerning direct relations with the project initiators (similar to DWF’s involvement in meme coins like PEPE and LADYS in the second quarter of this year).

In terms of financial data, CYBER’s performance was similar to that of YGG: contract data initially showed a surge in open interest and stable rates. This was followed by a slowing down in the growth of positions, a decline in rates in the medium term, and a reduction in positions due to longs taking profits later on.

On February 2, 2023, the DWF blockchain address received a transfer of approximately 4.12 million tokens from the official Coin98 address, equivalent to about $1.11 million based on the market price of the day (with the C98 secondary market price at about $0.27). These were immediately transferred to the Binance exchange. On August 8, Coin98 announced it had received a seven-figure investment from DWF Labs to promote widespread adoption of Web3. On October 12, media reports indicated that DWF transferred 1 million USDT to C98. Considering C98’s price performance, after DWF received the tokens and they were deposited on the exchange, C98 experienced a brief surge before entering a five-month decline. On August 8, following a media release, the price rallied by 58% within two days from its previous low before quickly falling again. In retrospect, this scenario may essentially have been DWF obtaining tokens from the C98 project team at a 10% discount, followed by selling on the secondary market for a profit.

Prior to its rally, C98’s data indicated a significant increase in positions. The end of the price increase phase was marked by a reduction in positions due to longs taking profits, accompanied by a return to regular fee rates.”

Other targets of similar price manipulation techniques include LEVER, WAVES, CFX, MASK, ARPA, etc.

The above are relatively typical targets of DWF’s recent operations. It can be seen that DWF often participates in both the futures and spot markets. In the early stages of market movement, a large influx of funds into the futures market is observed, as the main funds’ early contracts are bullish, thus the increase in positions does not affect the rates. The medium term is usually characterized by spot market boosting, where the main futures longs begin to close positions. This phase often presents as a surge in spot prices, severe negative futures rates, and stagnant or decreasing positions. Some targets may experience a final surge in price, creating liquidity and enabling the main spot market players to secure better exit prices and liquidity. After the main futures longs have closed their positions and taken profits, the market trend for some targets may end immediately. It is crucial to determine whether the continued price increase in the spot market in the final stage will generate profits for the main players that exceed costs (such as whether there are key resistance levels overhead and if significant selling pressure exists on the trading floor).

1. “Marketing-style” investments and on-chain transfers, utilizing brand image to create positive news to conceal the nature of their sell-offs.

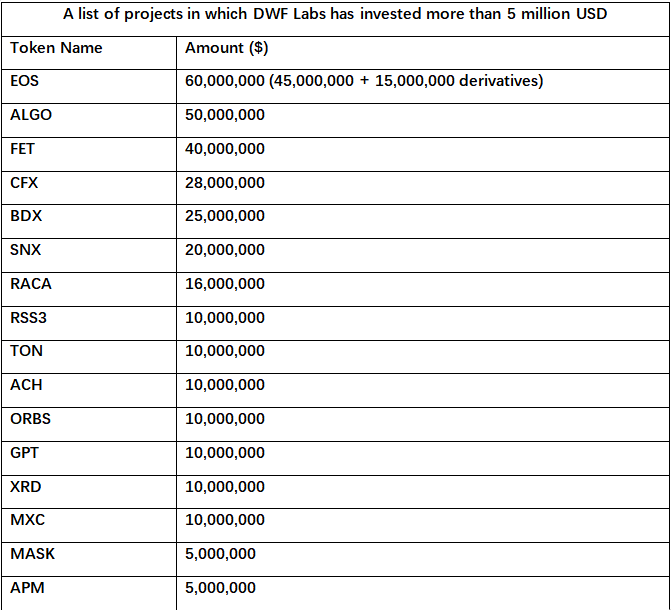

DWF, as a newly entered investment institution, has been actively involved during the bear market, collaborating on more than 260 projects. According to media reports, DWF has invested in over 100 projects, including numerous large-scale investments. To summarize, their investments in projects exceeding 5 million U.S. dollars are:

Grachev, the Co-Founder of DWF, has indicated that DWF Labs operates without external investors. However, its frequent and substantial investments have not only caused the market to question the origins of its capital but also raised eyebrows regarding the choice of its investments. Most projects backed by DWF are not trending within the industry. Instead, they are typically older projects with average or below-average fundamentals, such as EOS and ALGO, among others. Following DWF’s widespread investments, there has been no noticeable improvement in these projects’ product development, market promotion, or community collaboration.

It is speculated that some of DWF’s actions might be “marketing-style” investments, intended to create favorable conditions to attract retail investors. This strategy potentially involves repeatedly hyping the coin prices in the secondary market, facilitating the team’s token sales. For instance, despite announcing a $40 million investment in FET, to date, DWF has only received approximately $3 million in tokens.

Additionally, on September 8, a blockchain address associated with DWF received a PERP transfer from Binance. This transfer occurred after PERP had already seen several-fold increases. Following the appearance of withdrawal activities from exchanges related to DWF, there was a significant uptick in PERP buying, momentarily driving up the price before a substantial sell-off led to a downturn, concluding the market hype.

On October 17, BNX announced a strategic collaboration with DWF. Prior to this announcement, BNX had experienced a significant increase over a week. However, immediately after the information was released, there was a rapid sell-off, suggesting the likelihood of insider trading, utilizing DWF’s brand effect to create news, generate liquidity, and offload holdings.

There are numerous instances where project teams, in collaboration with DWF, have exploited its brand influence to create positive news, attract liquidity, and facilitate sell-offs. Participants in the secondary market need to exercise caution and discernment when encountering information related to DWF, as many assets associated with DWF, such as EOS, CELO, FLOW, and BICO, continue to experience a decline in prices.

1. Seeking “distressed” projects and taking advantage of the difficult financing conditions during a bear market allows DWF to wield significant bargaining power and maximize profits.

Abracadabra (SPELL) is a stablecoin project collateralized by interest-bearing assets (such as stablecoin LPs in Curve, stablecoin deposit certificates in Yearn, etc.). After experiencing the “UST debacle” (where UST, once a key underlying asset of Abracadabra, collapsed, leaving Abracadabra with a significant amount of bad debt) and a prolonged bear market that saw a contraction in the market value of stablecoins, the protocol’s Total Value Locked (TVL), token price, and overall market performance have consistently stagnated, making sustainable development challenging. On September 14th, the AIP#28 proposal was passed, stipulating the introduction of DWF as a market maker for SPELL, with the following market-making terms:

1. Abracadabra provides DWF with a 24-month SPELL loan of 1.8 million USD.

2. DWF will purchase tokens worth 1 million USD from the DAO at a 15% discount to the market price, with this specific share locked for 24 months.

3. Abracadabra pays DWF a European-style call option as market-making fees, exercisable after the loan period.

Compared to other market-making initiatives in the industry, the cost borne by the Abracadabra project under these terms is conspicuously higher, including discounted token purchases and European call options. Given the terms, which include token purchases at a market discount, it stands to reason from DWF’s perspective that depressing the token price in the short term serves to maximize their benefits. In line with market performance, the price of SPELL has been on a downturn since DWF’s involvement. Here are the details:

Voting on the proposal began on September 11th and passed on September 14th. Influenced by this development, the price of SPELL increased from a low of 0.0003716 on September 11th to a high of 0.0006390 on September 19th, a maximum rise of 72% (speculated by market forces).

On September 19th, Abracadabra provided DWF with 3.3 million SPELL loans. Subsequently, DWF transferred this to Binance, and SPELL began its downward trajectory, currently priced at 0.0004416, a 31% decrease from the previous high.

Capital flow data also reveals that during SPELL’s short-term market movements, there was a lack of consistency in funding. The 70% price increase was driven by a relay of multiple capital sources, indicating high uncertainty.

In summary, DWF initially built its brand image by creating a wealth effect through market manipulation in its early stages. It emerged as a product of weak regulatory oversight during a bear market, capitalizing on the development dilemmas of project teams and the psychology of retail investors in the market to profit from both ends. Project parties in the bear market generally face difficulties in liquidation and financing, and direct token sales can undermine the fragile market confidence, significantly depress token prices, and affect the project’s ecosystem. Under these circumstances, DWF appears as a bridge for project parties to sell tokens, assisting in offloading through OTC or other marketing means. For instance, describing the behavior of OTC token acquisitions from project parties as strategic investment, it has actually not been observed to provide substantial assistance for the long-term development of the projects. Instead, it quickly resells the tokens, concealing the nature of project parties’ disguised unloading through publicity and packaging, and DWF also profits from both project parties and users in this process.

For secondary market investors, upon seeing information about a project’s collaboration with DWF, it is essential to first distinguish which DWF business it belongs to (secondary investment, OTC, market making, marketing) and apply different strategies accordingly. Based on past market performance:

1. Targets involving DWF’s direct participation in secondary market investments need special attention. Such targets are usually newly-listed coins with a good structure of chips, or Memes.

2. Targets for which DWF purchases tokens OTC from project parties (packaged as strategic investments) tend to show a price decline in the secondary market for several months, followed by a rapid market pull, ending after DWF deposits tokens to the exchange (the market pull typically lasts no more than one week).

3. DWF’s genuine market-making projects do not have doubling scenarios, but they usually attract speculative capital and offer a brief window for position building, providing an opportunity to take a step ahead.

4. Market trends triggered by DWF-related marketing news have a relatively poor success rate and risk-reward ratio. The underlying logic is that interested parties use DWF’s current market influence to attract liquidity and dump their positions. Once it is determined that DWF intends to manipulate the market, explosive increases in contract positions and spot transaction volumes signal the start of market movements. Interactions between DWF’s on-chain addresses and exchange addresses (at high prices), decreases in holdings, and extremely negative funding rates often indicate the end of market trends.

LD Capital

As a global blockchain investment firm, we have built a portfolio of over 250 investments since 2016, spanning across various sectors, including infrastructure, DeFi, GameFi, AI, and the Ethereum ecosystem. We focus on investing in projects with disruptive innovations, actively taking on the role of primary investors, and providing comprehensive post-investment services to these projects. We employ a combination of direct investment from our own funds and a distributed fund model to cover all-stages of investment.

Trend Research

Trend Research division specializes in crypto hedge funds focusing on secondary areas within the crypto market. Our team members come from platforms and institutions like Binance and CITIC. We excel in macroeconomics, industry trends, and project data analysis. With funds dedicated to trend funds, index funds, hedge funds, and liquidity funds, we manage assets totaling over $400 million, including proprietary assets.

Cycle Ventures

We are a specialized early-stage investment firm in Web3, focusing on investment and service, with a strong emphasis on three major areas: Infra, AI, and Dapp. We have a team of nearly 20 senior engineers and dozens of crypto experts as advisors, deeply assisting projects in strategic design, technical development, and liquidity enhancement. We are deeply involved with asset management agency Cycle Digital and liquidity service provider Cycle Trading. Also, the team is actively involved with X Labs, a compliance service institution in Hong Kong, to help global projects establish a presence in Hong Kong and ensure compliance.

website: ldcap.com

twitter: twitter.com/ld_capital

mail: BP@ldcap.com

medium:ld-capital.medium.com